For our customers sourcing globally, tariff introductions significantly affect import costs and overall impact on margins if not repositioning or increasing pricing otherwise. Companies need to start thinking about how they will perform price changes if required and how to track the related tariff cost independently from the supplier cost.

When tariffs are implemented, NetSuite can improve a company's supply chain by providing enhanced visibility into inventory levels, facilitating supplier diversification, automating landed cost calculations, leveraging advanced analytics to identify cost-saving opportunities, and enabling better communication with suppliers to manage potential disruptions through its integrated platform proactively.

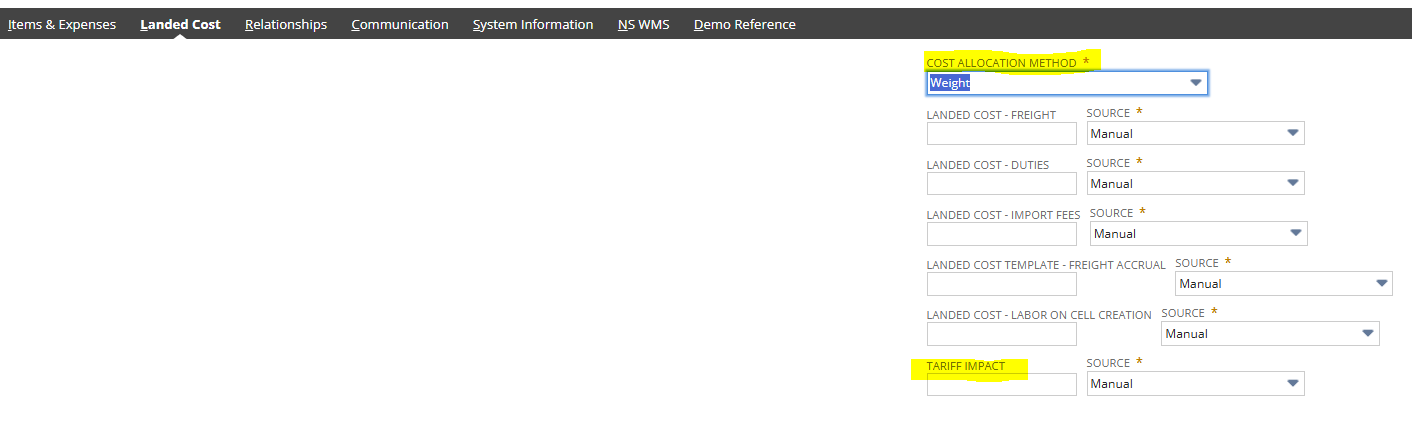

Once tariffs are implemented and if other sources are not available or present a cost or lead-time advantage the Company will need to set a strategy to track the related cost. A very good solution to this issue is to enable Landed Cost tracking at the item level and create a related Landed Cost Category (named Tariff Impact, for example) and be able to capture the related cost when receiving inventory on an Item Receipt transaction. As with any other landed cost category, this can be applied to the impacted items on the Item Receipt using one of three distribution methods: Weight, Quantity, and Value.

- Create a GL account that you want to track the related impact of tariff cost.

- Create a Landed Cost Category and link to the related GL expense account

- When receiving the item, select the Landed Cost tab and define the method to distribute the cost, input related costs for each defined Landed Cost Category

You can also create Landed Cost Templates that will automatically create the related cost if the categories intended to capture are not of a variable nature.

The result of applying the Landed Cost will be a direct cost increase on the average cost per item.

Depending on the Costing Method used for the inventory, if you use Standard Costing, NetSuite will help identify cost variations from the defined Standard Cost:

- Standard Cost: A predetermined cost assigned to an inventory item, which is used as a benchmark to compare against the actual cost, allowing you to identify variances.

- Variance Calculation: When a purchase is received, the system compares the landed cost of the item to the standard cost, generating a variance amount that can be either favorable (actual cost lower than standard) or unfavorable (actual cost higher than standard).

How to use landed cost and standard cost reporting variances in NetSuite:

- Monitor Inventory Costs: By analyzing variances, you can identify areas where cost savings can be achieved, such as negotiating better shipping rates or optimizing customs processes.

- Improve Budgeting: Understanding variances helps in more accurate budgeting by adjusting standard costs based on historical data and anticipated cost changes.

- Performance Analysis: By comparing actual landed costs to standard costs, you can assess the efficiency of your procurement and inventory management processes

Talk to a NetSuite Expert

Tell us what you're working on, and we'll help you figure out the next step.